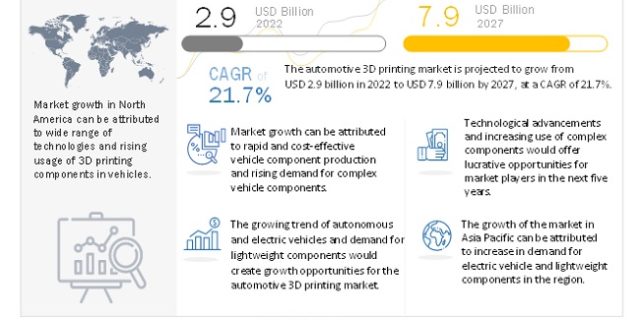

The 3D Printing in Automotive Industry is projected to grow from USD 2.9 billion in 2022 to USD 7.9 billion by 2027, at a CAGR of 21.7%. The increase in demand to reduce vehicle weight, production cost, and development time and increasing initiatives & investments by major OEMs are the major factors driving the growth of the 3D printing in automotive industry.

New product developments by OEMs, increase in demand for CASE vehicles, need for low-cost manufacturing, low-volume parts production, complex structured components, and critical engine components that are difficult to produce with conventional manufacturing methods are also the driving factors for the increasing development of additive manufacturing.

The prototyping and tooling segment is expected to register the largest share in the market. This has been ever-growing over the years and is predicted to grow in the future as well. Primarily the main reasons for this are the quick production of the prototype, fairly easy process, cost reduction, choices of filaments that could be used, agility to design changes, and reduced wastages. When compared to conventional practices, the prototypes could now be produced with the shortest possible lead times and minimal expense and wastage. The design can be modified anytime easily as only a final CAD design is sent for printing. The prototypes can now be made using different materials that can be tested on different criteria and environments, as there are wider options of filament materials to choose from.

Plastic is expected to register the largest share in 3D printing in automotive industry. The key reason is that plastic 3D printing technologies have been in the market for a long time, and most automakers have incorporated plastic 3D printing into their production. The various types of plastic materials that are used for 3D printing are Acrylonitrile Butadiene Styrene (ABS), nylon, polylactic acid, and others. The applications of plastic printed parts in automotive include dashboard components, housings, brackets, and several other interior and exterior components.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=250218997

The Stereolithography (SLA) has the largest market share among the 3D printing technologies. This technology provides various advantages in speed, cost-effectiveness, flexibility, and precision. Secondly, selective laser sintering (SLS) in automotive 3D printing is the technology that is expected to grow at a significant CAGR. The reason why the technology is growing is because it helps in building more strong and durable parts than other technologies. Another reason is that SLS is used in various applications from low-volume production to rapid prototyping. SLS can be used for printing various types of materials such as polymers, metals, ceramics, and even composites. Structurally complex components can also be printed using SLS. However, its scalability of printing multiple parts simultaneously is making it a preferred choice for automotive manufacturers, thereby boosting productivity.

3D printing has penetrated several new industries in a short span and is rapidly entering new application areas. The emergence of new applications for 3D printing has prompted industrialists and governments across the world to take notice of the technology. Several governments such as the US, the UK, China, Singapore, and Japan are undertaking initiatives and providing funding to educational institutions, research centres, and research and technology organizations (RTOs) to avail the opportunities provided by 3D printing and encourage the development of the same.

North America is estimated to hold the largest share of the global 3D printing market in 2022; this can be attributed to the continuous technological advancements in this field and the presence of hundreds of carmakers in the region.

The US is home to many global OEMs such as Ford Motor Company, General Motors, and so on. Thus, 3D printing has a significant market share in the US automotive industry. The recent development of electric vehicles and their R&D require more additive manufacturing technologies. In addition, growing installation of premium features in passenger vehicles will lead to a greater number of 3D-printed parts in these vehicles in the US. The US is estimated to lead the plastic 3D printing market. The main reason for this is the presence of hundreds of carmakers in the country whose R&D and components such as interior trims, dashboards, and exterior components demand plastic additive manufacturing technology.

The European market is expected to exhibit growth in electric and autonomous vehicle production in the coming years, resulting in an increase in demand for 3D printing.

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=250218997