According to a new report by MarketsandMarkets™ – Clinical Communication & Collaboration Market in terms of revenue was estimated to be worth $2.6 billion in 2024 and is poised to reach $4.8 billion by 2029, growing at a CAGR of 13.2% from 2024 to 2029.

The growth in the clinical communication and collaboration market is driven by high prevalence of chronic diseases, rising prominence of big data and mHelath tools, and stringent regulatory requirements and industry standards. Moreover, transition towards value-based care and population health management further increases the significance of clinical communication and collaboration solutions. Thus, the the growing emphasis on interoperability and data exchange within healthcare ecosystems is expected to drive the integration of clinical communication and collaboration market during the forecast period.

Download an Illustrative overview: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=118830286

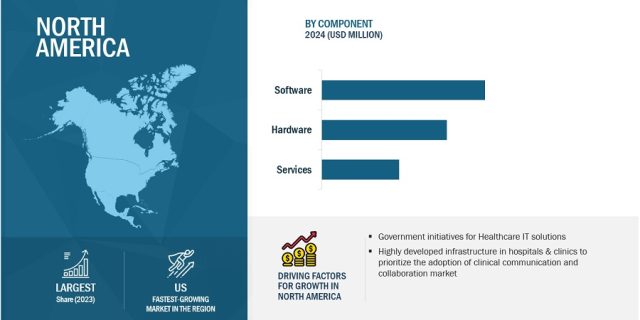

On the basis component, the Clinical Communication and Collaboration market is segmented into hardware, software and services segment. The software segment accounted for the largest share of the component segment in 2023. The software segment comprises of clinical alerting & notification, physician & nurse scheduling systems, telehealth platform, collaborative care platforms. The clinical alerting & notification segment held the largest market share in the software segment. These systems plays a pivotal role in enhancing patient safety, as it reduces response times, and improves clinical decision-making. Moreover, the increasing focus on care coordination and continuity across healthcare settings has propelled the demand for robust clinical alerting and notification solutions. Owing to the many benefits of the software solutions, several healthcare providers are increasingly adopting these solutions for smooth workflows and enhanced quality care.

Based on application, the Clinical Communication and Collaboration market is segmented into lab & radiology communication, nurse communication, patient communication & emergency alerts, physician communication. The physician communication segment held the largest market in 2023 due to its pivotal role in facilitating effective care delivery and enhancing care coordination. Moreover, the unique communication needs of physicians, including the requirement for secure and confidential communication channels, further highlights the importance of dedicated physician communication solutions within the clinical communication and collaboration market. These solutions offer encrypted messaging, secure voice and video calling, and other advanced features tailored to the specific requirements of healthcare providers, enabling them to communicate effectively while adhering to stringent privacy and security regulations.

Based on end users, the Clinical Communication and Collaboration market is segmented into hospitals & clinics, ambulatory surgical centers, long-term care facilities, nursing centers and other end-users which includes maternity care centers & fertility centers, and trauma and emergency care centers. The hospitals & clinics held the largest share among the end-users in 2023. From emergency departments and operating rooms to inpatient units and outpatient clinics, healthcare providers in hospitals and clinics rely heavily on effective communication channels to coordinate care plans, consult with colleagues, and ensure continuity of care for patients. As healthcare organizations continue to prioritize communication solutions that enhances care coordination, streamlines workflows, and support remote care delivery, hospitals and clinics are poised to remain key drivers of innovation and growth in the clinical communication and collaboration market.

The Clinical Communication and Collaboration market is segmented into five major regional segments, namely, North America, Europe, Asia Pacific, Latin America, and Middle East and Africa. In 2023, North America accounted for the largest share of the Clinical Communication and Collaboration market. This region’s dominance is due to highly developed healthcare infrastructure characterized by advanced technology adoption, robust regulatory frameworks, and a strong emphasis on patient-centric care delivery. Moreover, the presence of key market players such as Avaya LLC (US), Oracle (US), Cisco Systems, Inc. (US), Microsoft Corporation (US) among others are a key factor contributing to the growth of the region.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=118830286

Clinical Communication & Collaboration Market Dynamics:

Drivers:

- Advantages of clinical communication solutions in enhancing patient care and safety

Restraints:

- High investments required to build IT infrastructure

Opportunities:

- Growing opportunities in emerging markets

Challenge:

- Data security issues

Key Market Players of Clinical Communication & Collaboration Industry:

Prominent players in the Clinical Communication and Collaboration market include Avaya LLC (US), Oracle (US), Cisco Systems, Inc. (US), Microsoft Corporation (US), Baxter International (Hillrom) (US), symplr (US), NEC Corporation (Japan), Spok Inc. (US), Vocera Communications (Stryker) (US), Ascom Holding AG (Switzerland), Everbridge (US), Hidden Brains InfoTech. (India), Imprivata, Inc. (US), CommuniCare Technology, Inc. d/b/a Pulsara (US), Mobile Heartbeat (C-HCA, Inc.) (US), OnPage. (US), HARRIS ONPOINT (US), Jive Software, LLC (US), TigerConnect (US), JCT Healthcare Pty Ltd. (Australia), Amplion (US), AndorHealth (US), PerfectServe, Inc. (US), QliqSOFT, Inc. (US), and Connexall, GlobeStar Systems Inc. (Canada).

Breakdown of supply-side primary interviews, by company type, designation, and region:

- By Company Type: Tier 1 (40%), Tier 2 (35%), and Tier 3 (25%)

- By Designation: C-level (35%), Director-level (45%), and Others (20%)

- By Region: North America (55%), Europe (20%), Asia Pacific (15%), Latin America (5%) and Middle East Africa (5%)

Recent Developments of Clinical Communication & Collaboration Industry:

- In September 2023, Microsoft Corporation (US) collaborated with Mercy (US) to enable clinicians to revolutionize patient care through the use of generative AI.

- In August 2023, TeleVox (US) partnered with Oracle (US) to enhance its patient engagement solutions, leveraging OCI’s platform for improved communication in healthcare. As part of the Oracle PartnerNetwork (OPN), TeleVox on OCI delivers advanced capabilities for healthcare practices.

- In April 2023, Mobile Heartbeat (US) partnered with Akkadian Labs, LLC. (US) a leading developer of unified communications (UC) provisioning automation solutions. With this partnership, Mobile Heartbeat and Akkadian Labs aim to empower healthcare organizations with enhanced communication and collaboration capabilities, ultimately improving patient care outcomes.

Research Insights: https://www.marketsandmarkets.com/ResearchInsight/clinical-communication-collaboration-market.asp

Content Source: https://www.marketsandmarkets.com/PressReleases/clinical-communication-collaboration.asp