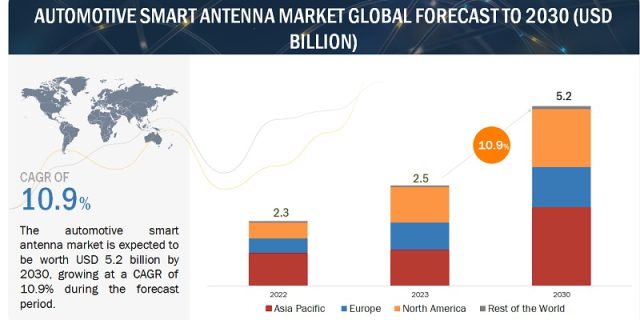

The automotive smart antenna industry is estimated to grow from USD 2.5 billion in 2023 to USD 5.2 billion by 2030, at a CAGR of 10.9%.

The demand for connected car features in mid-premium segment vehicles and EVs drives the automotive smart antenna industry. In addition, growing investments in the 5G infrastructure by key ISPs for high-speed connectivity, low latency, increased bandwidth, and network slicing create a conducive environment for the widespread adoption of smart antennas in vehicles.

“The ultra-high frequency automotive smart antennas would be the fastest-growing market.”

The ultra-high frequency segment is experiencing significant growth in the automotive smart antenna industry due to its higher data transfer rates offered by UHF antennas within the range of 4000 MHz to 6000 MHz. This capability is crucial for meeting the increasing demand for high-speed vehicle connectivity, supporting applications such as advanced driver-assistance systems (ADAS) and sophisticated infotainment systems. The adoption of 5G technology in the automotive industry is another major contributor to the popularity of UHF antennas. The new generation cellular network brings faster and more reliable communication, facilitating seamless connectivity between vehicles, infrastructure, and the cloud. This is particularly important for connected and autonomous vehicles that rely on low-latency and high-bandwidth communication for optimal performance. Products such as WB-1A from Antenna Systems and Towers, MA1559.A.001 and MA931.A.LBICGH.008 from Taoglas, 5-8 dBi 4G/5G External Magnetic High Gain Cell Antenna from Proxicast are some of the examples of ultra-high-frequency antennas which are offered in premium vehicles.

Various high-end vehicles, including luxury cars, electric vehicles, and those equipped with advanced connectivity features, are likely to incorporate UHF antennas. Manufacturers at the forefront of technological advancements are integrating these antennas to meet consumer demands for sophisticated vehicle communication systems. The increasing sales of connected and autonomous vehicles contribute to the growth of the smart antenna market, including those with ultra-high frequency capabilities. As consumer expectations for advanced vehicle features rise, manufacturers are incorporating more sophisticated communication systems to stay competitive. Luxury and high-end brands like Mercedes-Benz, Audi, and BMW increasingly incorporate UHF antennas for ADAS features like blind-spot monitoring and lane departure warning.

The automotive industry is witnessing a notable shift toward connected vehicles, emphasizing the importance of robust communication systems. With connectivity becoming a key selling point for vehicles, the demand for antennas capable of supporting high-frequency communication, such as UHF antennas, is expected to grow.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=29612374

“Light commercial vehicles are the second largest automotive smart antenna industry.“

LCVs are commonly used in these fleets for last-mile delivery and small-scale transportation. The demand for advanced connectivity solutions, including smart antennas, in LCVs can be driven by the need for real-time tracking, communication, and data exchange to optimize logistics operations. These antennas facilitate real-time vehicle monitoring, providing fleet operators with valuable insights into location, fuel efficiency, and driver behavior. Integrating smart antennas with telematics solutions allows LCVs to exchange critical data with fleet management platforms, enhancing operational efficiency. This data exchange enables businesses to optimize routes, improve fuel consumption, proactively schedule maintenance, and ensure compliance with regulatory requirements.

Moreover, with growing last-mile delivery services that require seamless communication between vehicles, central management systems, and delivery personnel, LCVs with smart antennas become a better choice. The result is a more connected and efficient logistics ecosystem where LCVs play a pivotal role in the evolving landscape of smart and data-driven transportation solutions. Companies like Geotab (UK), Verizon Connect (US), and Masternaut (France) provide advanced telematics solutions for LCVs. Companies like Amazon (US) and FedEx (US) rely on real-time vehicle tracking for their vast delivery vans and trucks. They utilize GPS data to optimize routes, monitor driver behavior, and ensure timely deliveries.

North America has the largest market share for LCVs. This region has a robust and expansive logistics & transportation industry, with a high reliance on commercial fleets for the efficient movement of goods. The convergence of advanced telematics and robust data exchange capabilities drives the increasing adoption of automotive smart antennas in the LCV segment.

“North America is the second largest market for smart antennas.“

North America is the largest manufacturer of light commercial vehicles, and the US is the region’s largest market for automotive smart antennas. Also, the US is home to the three major companies named Ford Motors, General Motors, and Fiat Chrysler, along with established European and Asian OEMs such as Toyota (Japan), Nissan (Japan), Honda (Japan), Hyundai/Kia (South Korea), BMW Group (Germany), and Volkswagen Group (Germany). All the OEMs are known for their passenger cars with advanced comfort and safety technologies. These manufacturers are meeting the increasing demand for automobiles by continuously increasing output, promoting the use of automotive smart antennas in automobiles for all vehicle types.

The US holds a significant number of vehicles manufactured in North America. Furthermore, vehicle sales in the US increased from 14.4 million in 2022 to 16.1 million in 2023. The sales of premium vehicles (E, F, and SUV – E) segment cars have increased by ~12.1%, from 1.6 million sold in 2022 to 1.8 million in 2023. Also, the sales of D-segment vehicles have increased in the US by ~4%, which was 4.1 million units in 2022 to 1.5 million in 2023. These premium vehicles offer features like enhanced lane departure warning and blind spot monitoring, cellular V2X system, telematics systems, dynamic route optimization, in-car Wi-Fi and internet access, and over-the-air software updates for sedan and premium vehicles. Hence, the increase in vehicle sales of D, E, and F segment vehicles in the US has contributed to the overall growth of smart antenna market.

Key Market Players

Major manufacturers in the automotive smart antenna industry includes major players in the market such as Continental AG (Germany), Denso Corporation (Japan), TE Connectivity (Switzerland), Forvia (France), and Ficosa Internacional SA (Spain).

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=29612374