This report aims to provide detailed insights into the global live

cell encapsulation market. It provides valuable information on the type,

procedure, application, and region in the market. Furthermore, the information

for these segments, by region, is also presented in this report. Leading

players in the market are profiled to study their product offerings and

understand the strategies undertaken by them to be competitive in this market.

Don’t miss out on business opportunities in Live Cell

Encapsulation Market

Revenue Growth Analysis:

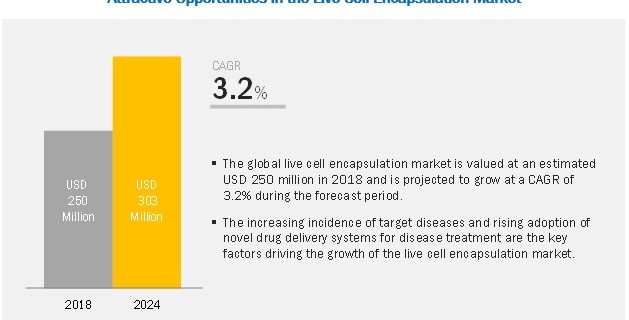

The global Cell Encapsulation Industry is projected to reach USD 303 million by

2024 from USD 250 million in

2018, at a CAGR of 3.2%.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=218019375

Key Factors Driving Market Growth:

The major factors driving the growth of the Live Cell Encapsulation Industry

are the rising public awareness related to the clinical role of encapsulated

cells in disease management, increasing public-private investments to support

product development, and the rising adoption of novel drug delivery systems for

disease treatment.

Simple dripping segment is expected to account for the largest share of the

Live Cell Encapsulation Market, by manufacturing technique, in 2018

Based on manufacturing technique, the Live Cell Encapsulation Industry is

segmented into . The instruments segment is expected to account for the largest

share of the Live Cell Encapsulation Industry in 2019. The increasing adoption

due to the procedural benefits (such as simple process, product

biocompatibility, and low particle size distribution) are the major factors

driving the growth of this market segment.

Alginate polymers segment estimated to be the fastest-growing polymer type

segment during the forecast period

Based on polymer type, the Live Cell Encapsulation Industry is segmented into

alginate, HEMA-MMA (hydroxyethyl methacrylate-methyl methacrylate), chitosan,

siliceous encapsulates, cellulose sulfate, PAN-PVC [poly (acrylonitrile vinyl

chloride)], and other polymers. The alginate segment is expected to grow at the

highest CAGR during the forecast period primarily due to the procedural

benefits such as uniform cell structures and high mechanical stability.

Drug delivery to account for the largest share of the Live Cell

Encapsulation Market, by application, in 2018

Based on end user, the Live Cell Encapsulation Industry is segmented into drug

delivery, regenerative medicine, cell transplantation, probiotics, and

research. Drug delivery are estimated to be the largest application of live

cell encapsulation, and this trend is expected to continue during the forecast

period. The large share of this application segment can be attributed to the

ongoing technological advancements in the field of cell encapsulation and

increased product affordability, and usage of biocompatible immobilization or

isolation systems.

Request Sample Report:

https://www.marketsandmarkets.com/requestsampleNew.asp?id=218019375

North America to

dominate the Live Cell Encapsulation Market during the forecast period

The Live Cell Encapsulation Industry is segmented into five major regions,

namely, North America, Europe, the Asia Pacific, Latin America, and

the Middle East and Africa. North America is

estimated to be the largest regional market for live cell encapsulation in 2019

majorly due to the increasing clinical data for the efficacy of the cell

encapsulation technique and the rising adoption of cell encapsulation

techniques among medical professionals.

Key Players:

The major players operating in the Live Cell Encapsulation Industry are

BioTime, Inc. (US), Reed Pacific Pty Ltd. (Australia), Viacyte, Inc. (US), Neurotech

Pharmaceuticals, Inc. (US), and Living Cell Technologies Ltd. (Australia) were the

top five players in the global Live Cell Encapsulation Industry.

Other prominent players operating in this market include Merck KGAA (Germany), Sigilon

Therapeutics, Inc. (US), Encapsys, LLC (US), Evonik Industries (Germany), Lycored (Israel), MiKroCaps

(Slovenia),

BÜCHI Labortechnik AG (Germany),

Blacktrace Holdings Ltd (UK), Sernova Corporation (Canada), and Balchem Corporation (US),

among others.