The ADAS market is projected to grow from 359.8 million units in 2025 to 652.5 million units by 2032 at a CAGR of 8.9%.

The ADAS market is undergoing a significant transformation, driven by the shift toward integrated domain controllers and high-performance, low-power computing systems capable of supporting the complex requirements of autonomous driving. Currently, most new vehicles are equipped with Level 1 or Level 2 ADAS features, which have become mainstream, establishing ADAS as the foundation for autonomous vehicles. NCAP safety ratings, which reward vehicles with advanced safety features like ADAS technologies with higher or 5-star ratings, are encouraging OEMs to integrate these systems into their vehicle models. At the same time, the declining costs of LiDAR, radar, and camera systems are enabling the broader deployment of multi-sensor ADAS suites in mass-market vehicles. Technological advancements in edge computing and specialized SoCs are enhancing onboard data processing capabilities, reducing latency and reliance on cloud connectivity. Moreover, the integration of ADAS with commercial vehicle telematics, fleet management, and V2X communication is creating new revenue opportunities in all vehicle segments.

“Lane departure warning system is projected to account for the largest share of the ADAS market during the forecast period.”

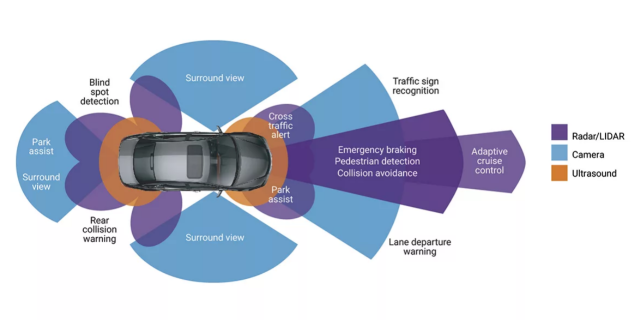

Lane departure warning (LDW) is projected to account for the largest share of the ADAS market by system type. The growth of LDW systems is primarily driven by the alarming rise in road accidents and the implementation of stringent safety regulations that mandate LDW integration into new vehicles. Additionally, automotive OEMs’ emphasis on reducing side-swipe and single-vehicle crashes, coupled with advancements in cost-effective camera and radar sensor technologies, has accelerated LDW deployment. Many vehicle models launched in 2025 come equipped with LDW as a standard feature, often combined with lane keep assist (LKA). For instance, the 2025 Chevrolet lineup includes LKA with LDW, which monitors the vehicle’s position within the lane using cameras and sensors. If the system detects unintended lane departure without signaling, it provides an audible alert and may gently steer the vehicle back into its lane. Further, government regulatory bodies are introducing regulations to mandate LDW systems for improved road safety. For instance, in November 2024, NHTSA updated its NCAP to include LDW in safety evaluations, while in March 2025, India’s MoRTH proposed that from April 2026, all new passenger vehicles designed to carry more than eight passengers must include ADAS features such as LDW.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1201

Based on level of autonomy, the L3 segment is projected to grow at the fastest rate during the forecast period

Often referred to as ‘eyes-off’ vehicles, L3 vehicles can allow the driver to sit back and relax as the car can take care of everything while driving along the road. The rapid progress and declining costs associated with ADAS components and solutions are anticipated to catalyze growth within the ADAS market. L3 automation has been limited to specific regions in Europe, primarily within geofenced areas, where the system operates under controlled conditions. For instance, in December 2024, Mercedes-Benz expanded its DRIVE PILOT Level 3 system in Germany, now supporting automated driving at a speed of up to 95 km/h on designated highways. This system allows drivers to disengage from active driving under specific conditions, enhancing comfort and safety within approved operational areas.

“North America is estimated to hold the second-largest share of the ADAS market during the forecast period.”

North America is expected to be the second-largest ADAS market during the forecast period. The emergence of higher autonomy vehicles stands out as a pivotal trend within the North American ADAS market. Numerous companies are actively engaged in the creation of self-driving cars, necessitating sophisticated ADAS. For instance, in April 2025, Volkswagen AG partnered with Uber to introduce thousands of electric self-driving vans in the US. The vehicles will be equipped with autonomous driving technology, with commercial operations expected to begin in Los Angeles by 2026. The increasing interest in autonomous vehicles is expected to propel the ADAS market expansion in the foreseeable future as further advancements in technology are made and incorporated into vehicles. Additionally, government regulations mandating the adoption of these technologies are expected to contribute to market growth. For instance, in April 2024, the National Highway Traffic Safety Administration (NHTSA) finalized Federal Motor Vehicle Safety Standard (FMVSS) No. 127, mandating that all new light vehicles (weighing 10,000 pounds or less) be equipped with automatic emergency braking (AEB), pedestrian AEB (PAEB), and forward collision warning (FCW). The rule is set to take effect in September 2029. In November 2024, NHTSA updated its New Car Assessment Program (NCAP) to include evaluations of additional ADAS features, including lane keeping assist (LKA), enhanced lane departure warning (LDW), blind spot detection and intervention, and pedestrian AEB. These additions aim to provide consumers with more comprehensive safety information and encourage manufacturers to adopt advanced safety technologies.

Recent Developments of ADAS Market

- In April 2025, Continental’s Automotive Group Sector was renamed ‘Aumovio’ after its planned spin-off and IPO in September 2025. As an independent company, Aumovio will focus on advanced electronic and mobility solutions to support safe, connected, and autonomous driving. Its offerings will include sensor systems, smart displays, braking and comfort technologies, as well as software platforms and assistance systems for software-defined and autonomous vehicles.

- In April 2025, Mobileye (Israel) partnered with Valens Semiconductor (Israel) for ADAS projects. Valens’ VA7000 chipsets, which follow the MIPI A-PHY standard, will be used to create the in-car connectivity system between sensors and computing units for Mobileye’s EyeQ6-based advanced and autonomous driving programs.

- In April 2025, Valeo (France) partnered with Renault Group (France) to equip the latest Renault Grand Koleos model with the Valeo Smart Safety 360 (VSS360) system. VSS360 is a new Turnkey L2/L2+ driver assistance system that provides driving safety and parking assistance functions. It includes a smart front camera, radars, detection algorithms, and advanced features.

- In March 2025, Mobileye introduced Surround ADAS, a software-defined system that enables hands-off, eyes-on driving at a lower cost. It uses Mobileye’s advanced software developed for autonomous vehicles and runs on a single EyeQ6 High SoC. The system uses up to 11 sensors, including multiple cameras and radars, and combines technologies like AI, computer vision, REM crowdsourced mapping, driving policy, and over-the-air updates. Key features include hands-off driving on highways and selected roads at speeds up to 130 km/h, surround collision avoidance, lane support, low-speed acceleration control, automatic lane changes, smart parking, and driver monitoring.

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=1201